Introduction

Australia is entering 2026 with significant tax reforms aimed at simplifying the tax system and supporting economic growth. First, these changes will affect both individuals and businesses, impacting income tax, corporate obligations, and various deductions. Understanding these reforms is essential for planning finances effectively. Moreover, early preparation can help taxpayers maximize benefits and avoid penalties. In this article, we break down the key aspects of the 2026 tax reform and provide actionable strategies for individuals and business owners alike.

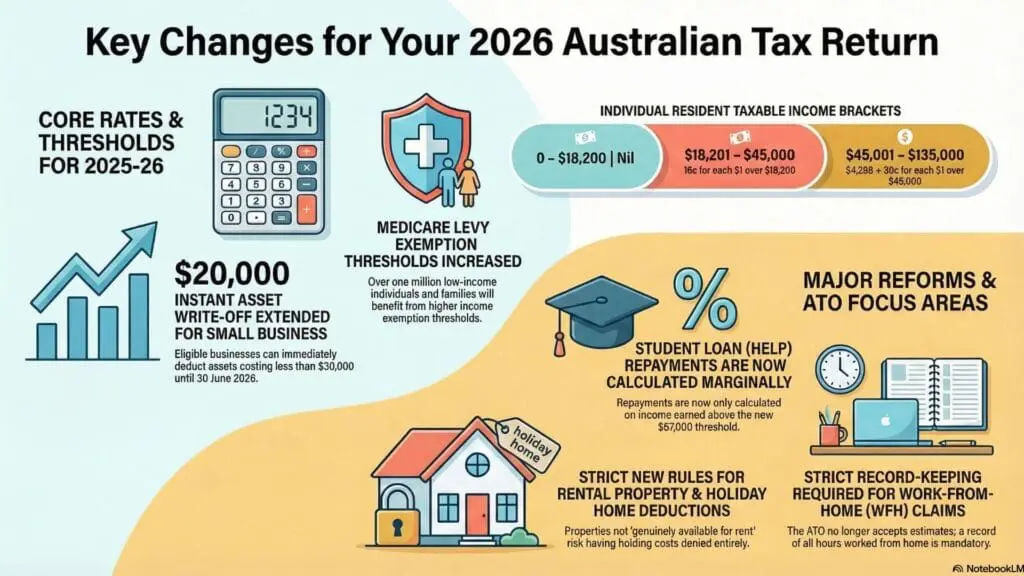

Overview of 2026 Tax Reform

Second, the 2026 tax reform focuses on three major areas: simplifying income tax brackets, adjusting corporate taxes, and updating deductions for businesses and individuals. According to the Australian Taxation Office (ATO), these measures aim to improve compliance, reduce complexity, and encourage investment.

Additionally, the government plans to introduce new reporting requirements for high-income earners and corporations. This includes enhanced digital reporting tools that streamline filing processes. For detailed official information, visit the Australian Taxation Office.

Finally, taxpayers must pay attention to transitional rules, as some reforms will be phased in over several months. Missing deadlines could result in fines or lost benefits.

In my experience, tax reforms often look simple on the surface but become complex during implementation. What matters most is understanding the transitional rules early, as this is where many taxpayers either gain unexpected benefits or face avoidable penalties.

Moreover, understanding broader economic conditions is essential for making smart investment decisions. For deeper insights, check our analysis on Australia’s economic outlook.

https://chipkie.com/blog/the-ultimate-2026-tax-guide-for-australia/

Impact on Individuals

Third, individuals will notice changes primarily in income tax brackets and deductions. For example, the threshold for the 32.5% tax rate may increase, reducing the tax burden for middle-income earners. Furthermore, deductions for education, medical expenses, and retirement contributions will be updated, which could either increase or decrease overall taxable income.

Additionally, digital filing tools introduced by the ATO will allow individuals to submit tax returns more efficiently. Those who plan their finances ahead of time can optimize deductions and credits. For instance, contributing additional funds to superannuation before the reform takes effect may provide tax advantages.

Finally, it is advisable to consult a tax professional to ensure compliance and maximize benefits. Ignoring minor changes could lead to unnecessary penalties or missed savings.

Personally, I’ve found that small adjustments like timing superannuation contributions or claiming overlooked deductions can make a noticeable difference in overall tax savings. Many people underestimate how much these minor strategies can add up over time.

Impact on Businesses

Fourth, businesses will experience notable changes in corporate taxes and reporting obligations. Small and medium-sized enterprises (SMEs) may benefit from reduced tax rates, enhanced depreciation options, and streamlined digital reporting. Conversely, large corporations will face stricter compliance requirements.

Moreover, the reform encourages investment by allowing accelerated write-offs for certain capital expenditures. Companies planning expansion or restructuring should consider the timing of investments to optimize tax benefits. According to Business.gov.au, early adoption of compliant reporting systems can prevent future issues.

Finally, staying informed on transitional rules and digital compliance tools is crucial for avoiding penalties and fines.

Strategic Planning

Fifth, strategic planning is essential for both individuals and businesses. Taxpayers should review their current financial position, assess which deductions and credits apply, and plan investments accordingly. For example, individuals can prioritize superannuation contributions, while businesses might accelerate capital purchases before the new rules take effect.

Additionally, leveraging accounting software compatible with the ATO’s digital systems can simplify compliance. Consulting a certified tax professional is strongly recommended to ensure all aspects of the reform are addressed efficiently.

Finally, staying updated with news and official announcements is key to avoiding unexpected tax liabilities and maximizing benefits.

From what I’ve observed, businesses that prepare early for tax changes tend to gain a competitive advantage. Delaying compliance or planning usually results in higher costs and missed opportunities, especially during major reforms like this.

Conclusion

In conclusion, the Australia Tax Reform 2026 introduces significant changes affecting income tax, corporate obligations, and deductions. First, individuals should evaluate income tax brackets and available credits to optimize personal finances. Second, businesses must consider corporate tax rates, reporting obligations, and investment timing. Third, leveraging professional advice and digital tools ensures compliance and maximizes benefits. Staying informed and proactive will allow taxpayers to navigate these reforms successfully.

Frequently Asked Questions (FAQ)

What is the Australia Tax Reform 2026?

The Australia Tax Reform 2026 introduces changes to income tax brackets, corporate tax rates, and deductions to simplify the system and support economic growth.

How will the 2026 tax reform affect individuals?

Individuals may benefit from adjusted tax brackets and updated deductions, potentially reducing overall tax liabilities depending on income and financial planning.

What changes will impact businesses in Australia?

Businesses may see reduced tax rates for SMEs, new reporting requirements, and opportunities for accelerated depreciation on investments.

Are there risks if I don’t prepare for the tax changes?

Yes, failing to understand transitional rules and deadlines could lead to penalties, missed deductions, or higher tax obligations.

What strategies can help optimize taxes under the new reform?

Key strategies include reviewing deductions, timing investments, contributing to superannuation, and consulting tax professionals for personalized advice.